IMF April 2026: 3.3% Global Growth — Upgrade With Warning

IMF raised global GDP to 3.3% but flagged Iran war, inflation, trade fragmentation and defense spending as severe risks.

Published: April 14, 2026

Photo: IMF via Atlas Current

Key Takeaways

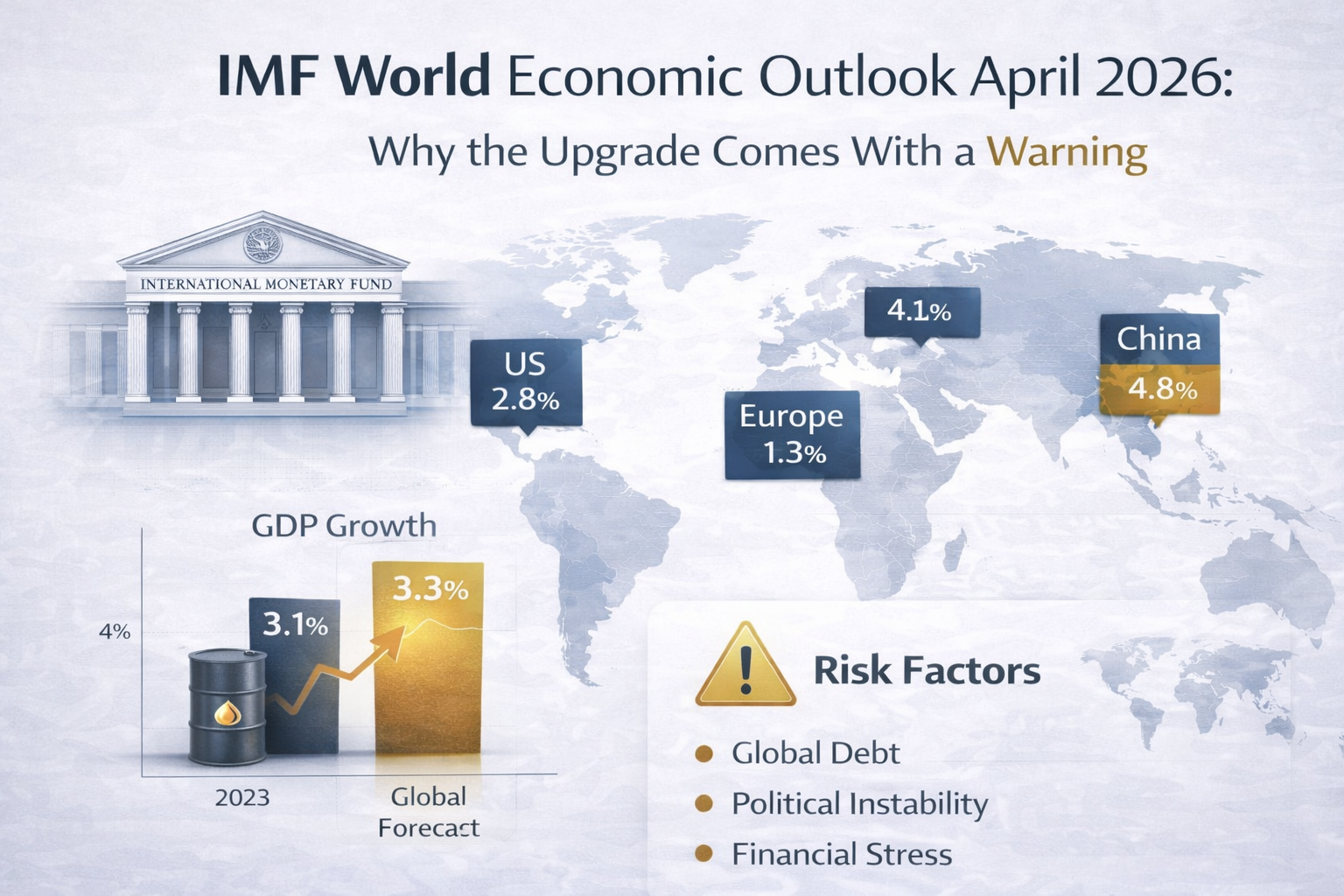

- IMF upgrades 2026 global GDP forecast to 3.3%, up 0.1 percentage points from the October 2025 report.

- Iran war described as the largest oil supply disruption in history, pushing crude above $95/barrel.

- Growth distribution rated 'sharply less equal' — half of developing economy spending goes to food and energy.

- Defense spending surging in emerging economies, crowding out social budgets.

- Vietnam projected at 6.5%+ growth; FTSE Russell upgrade serves as investment catalyst.

GDP Forecasts by Region

Comparison of GDP growth projections from the April 2026 WEO report. Data per official IMF publication.

| Region | 2025 | 2026 (F) | Change |

|---|---|---|---|

| World | 3.2% | 3.3% | +0.1 |

| United States | 2.3% | 2.8% | +0.5 |

| China | 4.5% | 4.8% | +0.3 |

| India | 6.3% | 6.6% | +0.3 |

| Euro Area | 1.0% | 1.3% | +0.3 |

| Japan | 1.1% | 1.0% | -0.1 |

| Vietnam | 6.1% | 6.5% | +0.4 |

| ASEAN-5 | 4.6% | 4.9% | +0.3 |

Source: IMF World Economic Outlook, April 2026. (F) = Forecast.

Iran War: Economic Fallout

Photo: IMF April 2026 WEO

The April 2026 WEO dedicates an entire chapter to the economic impact of the Iran conflict. The IMF describes it as 'the largest oil supply disruption in history,' surpassing even the 1973 oil crisis. Brent crude has been trading above $95/barrel, driving energy inflation sharply higher across all regions.

Net oil importers such as India, Thailand, and the Philippines face the heaviest pressure. Trade balances are deteriorating, foreign exchange reserves are narrowing, and central banks are forced to keep rates higher than expected to contain inflation.

Defense Spending Surge

A notable trend in the WEO is the defense spending boom across emerging economies. Middle East conflict and geopolitical tensions have pushed many nations to raise military budgets to 3–5% of GDP, crowding out spending on education, healthcare, and civilian infrastructure.

The IMF warns that diverting resources from development to defense will slow poverty reduction progress and increase long-term inequality. It is a vicious cycle: security instability demands defense spending, but defense spending reduces resources for sustainable development.

Inequality Warning

Distribution of global growth described as 'sharply less equal.' Advanced economies benefit from AI and automation, while low-income countries remain trapped in debt and energy dependency.

Half of developing economy spending goes to food and energy. When oil and food prices rise simultaneously, poor households are impacted 3–4x more than wealthy ones.

Photo: IMF / Atlas Current

Food & Energy Vulnerability

The IMF stresses that low-income countries are hardest hit by the dual price shock (oil + food). Many East African and South Asian nations face rising malnutrition as food subsidies are cut to offset energy budget shortfalls.

While rice exporters like Vietnam, Thailand, and India benefit from high rice prices, this burden falls on net food importers. The report calls on exporting nations not to restrict food exports to avoid repeating the mistakes of 2022.

Vietnam in the April 2026 WEO

Vietnam is projected by the IMF to achieve ~6.5% GDP growth in 2026, placing it among the fastest-growing economies in Asia. Key drivers include: surging electronics and semiconductor exports fueled by supply chain shifts from China, record FDI inflows from South Korea and Japan, and domestic consumption recovery.

Notably, the FTSE Russell upgrade of Vietnam to emerging market status (expected to finalize in 2026) is highlighted in the WEO as a significant catalyst, potentially attracting an additional $5–8 billion in portfolio investment flows.

What Does This Mean for Vietnamese?

A 15–20% global rice price increase is a major opportunity for farmers and export enterprises. However, domestic rice prices also get pushed up, affecting daily meals for low-income households.

Oil above $95/barrel will keep pushing domestic fuel prices higher. Transportation, logistics, and manufacturing all face cost pressure, driving up final goods prices.

Electronics and semiconductor exports remain a bright spot. Samsung, Intel, and Amkor are all expanding production in Vietnam. Record FDI, especially from South Korea and Japan, will create new jobs and advance industrialization.

Risks & Scenarios

The WEO identifies 5 key risks for the global economy in H2 2026. Expand each for details.

Frequently Asked Questions

References

- IMF — World Economic Outlook, April 2026

- Atlas Current — IMF World Economic Outlook April 2026 Summary

- Brookings — April 2026 TIGER Update: A Year of Peril

ZestLab analysis based on official sources as of April 14, 2026. Not investment advice.

Related Topics

Stay on top of trends

Bookmark this page and check back often for the latest updates and insights.