Smartphone Sales Face Record Crash in 2026

Global smartphone shipments are falling at the fastest pace ever recorded. The culprit is not weak demand for phones — it is the insatiable appetite of AI data centers devouring the world's memory chip supply.

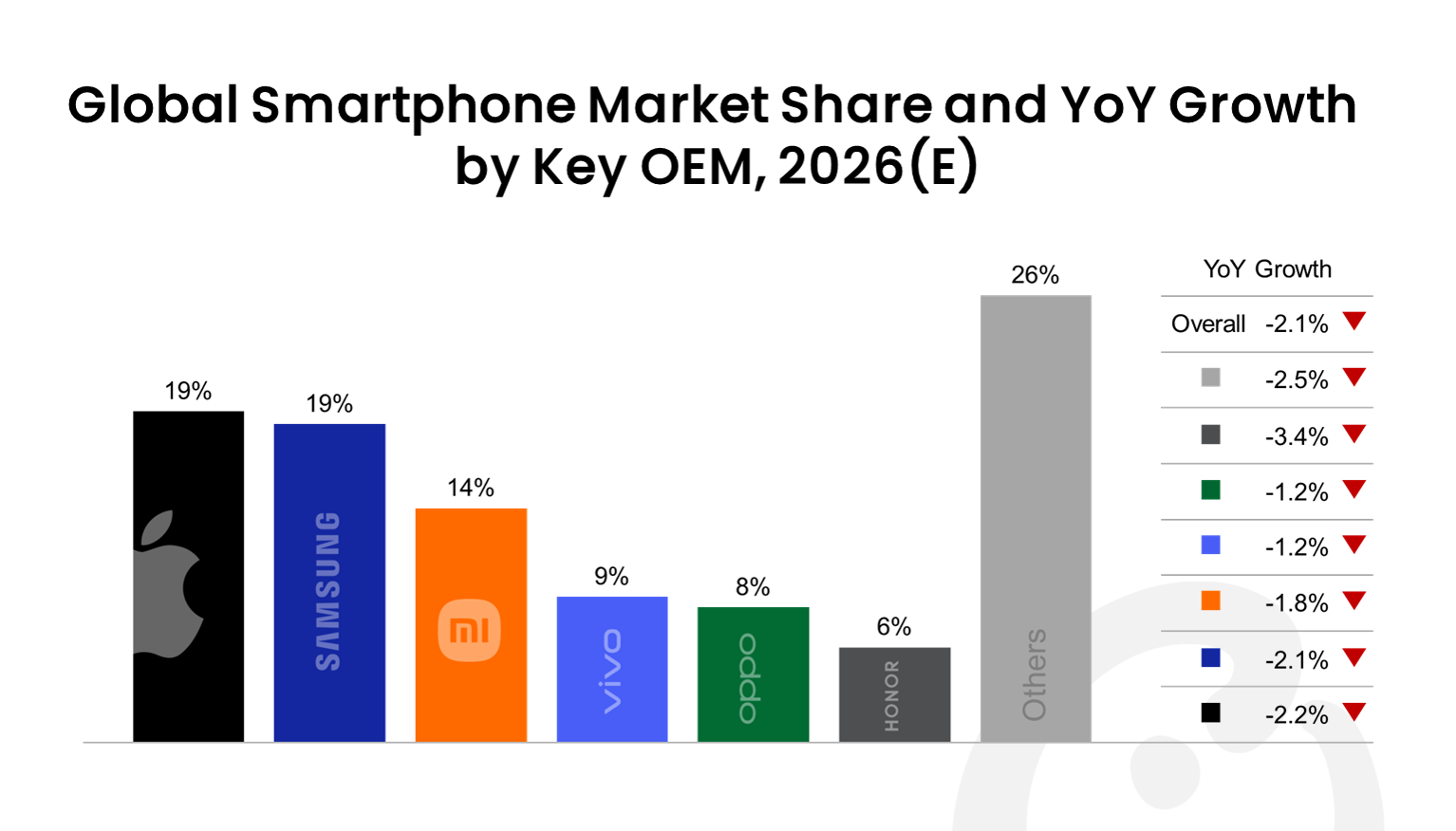

Key Takeaways

- IDC forecasts a 13% year-over-year decline to 1.12 billion units in 2026 — the sharpest contraction on record and the lowest volume since 2013.

- The root cause is not consumer apathy but a supply-side crisis: AI data centers operated by Meta, Google, and Microsoft are consuming so much DRAM that mobile-grade memory prices have surged 40%.

- Morgan Stanley slashed its 2026 smartphone forecast by 15%, while average selling prices are surging 14% to a record $523 as manufacturers pass on component costs.

- The budget segment (sub-$200) is being devastated — bill of materials up 20-30% with shipments down 31% — while premium ($800+) phones continue growing at roughly 4%.

- Samsung and Apple are best positioned to weather the storm thanks to vertical integration. Chinese OEMs like Xiaomi and Oppo face a margin squeeze as they lack in-house memory sourcing.

How AI Data Centers Are Starving Smartphones of Memory

Budget vs. Premium: Two Markets, Two Fates

| Budget (Sub-$200) | Premium ($800+) | |

|---|---|---|

| Shipment trend | -31% YoY collapse | +4% steady growth |

| BoM cost impact | +20-30% devastating | +8-12% manageable |

| Consumer response | Delaying upgrades | Trading up for AI features |

| OEM margin | Near-zero or negative | 15-25% healthy |

| Key players | Xiaomi, Realme, Transsion | Apple, Samsung, Google |

We are witnessing a historic reallocation of semiconductor resources from consumer electronics to AI infrastructure. The smartphone industry is collateral damage in the race to build artificial general intelligence.

Winners and Losers in the Memory Crisis

Samsung Electronics

Dual advantage: profits from selling expensive DRAM to AI clients while its Galaxy line absorbs cost increases better than rivals

Apple iPhone

Long-term memory contracts and massive purchasing power insulate iPhone from worst price spikes; premium demand intact

Xiaomi & Oppo

Squeezed hardest — reliant on spot-market memory purchases with razor-thin margins in the sub-$300 segment

Emerging Markets

Africa, India, and Southeast Asia hit hardest — affordable phones becoming less affordable, digital divide widening

Memory Makers (SK Hynix, Micron)

Record profits as AI demand pushes DRAM prices up 40% — but facing regulatory scrutiny over supply allocation

AI Giants (Meta, Google, Microsoft)

Securing memory at any price — their infrastructure buildout is directly responsible for the smartphone supply crunch

How the Crisis Unfolded

DRAM prices begin accelerating as AI orders surge

Samsung and SK Hynix announce major capacity reallocation from mobile to HBM3E server memory. Spot prices rise 15% in a single quarter.

IDC issues historic downgrade: -13% forecast

IDC revises 2026 global smartphone forecast from 1.29 billion to 1.12 billion units — the sharpest single-year downward revision in the firm's tracking history.

Morgan Stanley cuts forecast by 15%, warns of 'structural shift'

Analysts at Morgan Stanley downgrade the entire smartphone supply chain, noting that AI memory demand is not cyclical but structural — this is the new normal.

ASP hits record $523 as budget segment collapses

Average selling price surges 14% to an all-time high of $523. Sub-$200 shipments crater 31% while premium $800+ grows 4%. The smartphone market is bifurcating.

The AI Infrastructure Arms Race Behind the Shortage

This is not a demand problem — consumers want to buy phones. It is a supply allocation problem driven by the economics of AI. Memory makers are rationally choosing higher-margin AI customers over lower-margin mobile OEMs.

What Happens Next: Three Scenarios for 2027

Frequently Asked Questions

References

- Counterpoint Research — Global Smartphone Shipments Forecast Q1 2026

- CNBC — Smartphone Market Faces Record Decline as AI Devours Memory Supply (March 2026)

- Morgan Stanley via Dataconomy — Smartphone Forecast Cut 15% on DRAM Supply Crunch (February 2026)

- IDC via Developing Telecoms — Global Handset Shipments to Fall 13% in 2026 (January 2026)